CORRESP: A correspondence can be sent as a document with another submission type or can be sent as a separate submission.

Published on August 23, 2022

Gravitas Education Holdings, Inc.

4/F, No. 29 Building, Fangguyuan Section 1

Fangzhuang, Fengtai District

Beijing 100078

People’s Republic of China

August 23, 2022

VIA EDGAR

Mr. Nicholas Nalbantian

Mr. Donald Field

Division of Corporation Finance

Office of Trade & Services

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Re: | Gravitas Education Holdings, Inc. (the “Company”) |

Form 20-F for the Fiscal Year Ended December 31, 2021

Filed May 11, 2022

| File No. 001-38203 |

Dear Messrs. Nalbantian and Field:

This letter sets forth the Company’s responses to the comments contained in the letter dated July 26, 2022, from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) regarding the Company’s Form 20-F for the fiscal year ended December 31, 2021 filed with the Commission on May 11, 2022 (the “2021 Form 20-F”). The Staff’s comments are repeated below in bold and are followed by the Company’s responses thereto. All capitalized terms used but not defined in this letter shall have the meaning ascribed to such terms in the 2021 Form 20-F.

FORM 20-F FOR THE FISCAL YEAR ENDED DECEMBER 31, 2021

Item 3. Key Information, page 3

| 1. | Please revise the disclosure in the Introduction section on page 1 to remove the exclusion of Hong Kong and Macau from the definition of the PRC and China. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the following underlined disclosure in Introduction and make conforming adjustments throughout the annual report in its future Form 20-F filings:

“‘China’ or the ‘PRC’

are to the People’s Republic of China, excluding, for the purposes of this annual report only, including

Hong Kong, and Macau and Taiwan.”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 2

| 2. | We note the “Our Holding Company Structure and Contractual Arrangements with the VIE” section on page 3 discusses legal and operational risks associated with being based in or having the majority of your operations in China and that your business operations may be subject to complex and evolving PRC laws and regulations. We also note that this section is drafted from a hypothetical or theoretical standpoint versus discussing in detail the recent regulatory changes which drove the divestiture of your kindergarten business. Please revise to discuss in detail the relevant laws and regulations (including the Opinions of the State Council on Deepening Reform and Standardized Development of Preschool Education, the Regulations on the Implementation of the Law on the Promotion of Private Education, and the Preschool Education Law (Draft for Comments)) which directly impacted the company’s business, the company’s compliance with these new laws and regulations and all material financial impacts related to the divestiture. In this regard, we note certain information is contained on pages 99 and F-60 but given the significance of the divestiture a more fulsome discussion should be provided in this section. |

The Company respectfully advises the Staff that our commercial objective drove the divestiture of our PRC kindergarten business, which simultaneously advanced our compliance obligations. Fundamentally, the divestiture reflects a major strategic shift in the Company’s business to become a new educational services output platform, which at the same time serves as a proactive solution for the Company to comport with the regulatory trend regarding the early-education industry in China. In lieu of operating these kindergartens by ourselves, we provide educational services to them. This way, we transition from an asset-heavy business model, with high capital overhead and inherent operational risks, to an asset-light business model, with scalability and strong margin. We are well positioned to provide services to early educational institutions across the country as we leverage the experience and insights accumulated over 20 years of operating play-and-learn centers, kindergartens and student care centers domestically and abroad. The Company respectfully further advises the Staff that the Company’s current understanding of all material financial impacts related to the divestiture is sufficiently reflected by the information disclosed in the subsequent event of the consolidated financial statements contained in the Form 20-F, which will be added as cross-references as shown below.

Gravitas Education Holdings, Inc.

August 23, 2022

Page 3

In response to the Staff’s comment, the Company respectfully proposes to revise and include the following underlined disclosure in Item 3. Key Information as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“The divestiture of our PRC kindergarten business was mainly motivated by our commercial objectives. We planned on transitioning our business model to become an educational services output platform and would derive significant revenue through such transition. As a result of the divestiture, an aggregate amount of RMB158.5 million will be paid in installments to our subsidiaries as compensation for the termination of VIE agreements. Additionally, we have entered into a series of service agreements with a term of 15 years with the former VIE, at arm’s-length terms under which our subsidiaries will continuingly provide brand royalty, training, management IT system, recruitment, and curriculum design services to the former VIE and the kindergartens operated by them. For detailed information regarding all material financial impacts related to the divestiture, see ‘Item 5. Operating and Financial Review and Prospects—A. Operating Results—Financial Impact by the Divestiture’ and ‘Notes to Consolidated Financial Statements for the Years Ended December 31, 2019, 2020 and 2021—26. Subsequent Event.’

We face various risks and uncertainties

related to doing business in China. Our business operations are primarily conducted in China, and we are subject to complex and evolving

PRC laws and regulations. The PRC government authorities amend and/or issue the rules, regulations and guidelines regarding the preschool

education industry from time to time, such as the Opinions of the Central Committee of the Communist Party of China and State Council

on Deepening Reform and Standardized Development in Preschool Education issued in November 2018, the Implementing Regulations for

the Law for Promoting Private Education of the PRC newly amended and became effective on September 1, 2021, and the PRC Preschool

Education Law (Draft for Comments) promulgated on September 7, 2020, and has not officially become effective. According to the aforementioned

regulations, (i) private schools are divided into non-profit or for-profit private schools, (ii) social capital is not allowed

to control non-profit kindergartens or kindergartens that are sponsored by state-owned assets or collectively-owned assets, (iii) private

schools providing compulsory education shall not conduct any transaction with any related party. We are of the view that we are in material

compliance with the aforementioned regulations, which are currently and officially effective. However, there are substantial uncertainties

regarding the interpretation and application of current and future PRC laws and regulations, and the PRC regulatory authorities may take

a view that is contrary to the opinion of ours. We are also of the view that government enforcement of the aforementioned regulations

is strong, and the divestiture of our PRC kindergarten business aligned with the facts that (i) an increasing number of private kindergartens

directly operated by us were requested by local education authorities to transfer into public kindergartens that are sponsored by the

local education authorities or their designated entities, (ii) during the actual operation of some kindergartens that leased and/or

are leasing government properties, the lessors were and/or are not willing to renew the leases; (iii) we noticed some public news

reported that several private schools were donated to the government as a whole and turned into government-run schools. For

example Also, we face risks associated with regulatory approvals on offshore offerings, anti-monopoly regulatory actions,

and oversight on cybersecurity and data privacy, as well as the possible lack of inspection by the Public Company Accounting Oversight

Board, or the PCAOB, on our auditors pursuant to the announcement of the PCAOB issued on December 16, 2021. This may impact our ability

to conduct certain businesses, accept foreign investments, or list on a United States or other foreign exchange. These risks could result

in a material adverse change in our operations and the value of our ADSs, significantly limit or completely hinder our ability to continue

to offer securities to investors, or cause the value of such securities to significantly decline. For a detailed description of risks

related to doing business in China, please refer to risks disclosed under ‘Item 3.D. Key Information—Risk Factors—Risks

Related to Doing Business in China.’”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 4

| 3. | We note your disclosure that you are not a Chinese operating company but a Cayman Islands holding company and that you conduct our business in China through (i) your PRC subsidiaries and (ii) the former VIE and the new VIE with which you maintained contractual arrangements. Please disclose that this structure involves unique risks to investors. Your disclosure should acknowledge that Chinese regulatory authorities could disallow this structure, which would likely result in a material change in your operations and/or a material change in the value of your securities, including that it could cause the value of such securities to significantly decline or become worthless. Provide a cross- reference to your detailed discussion of risks facing the company as a result of this structure. |

In response to the Staff’s comment, the Company respectfully proposes to include the following underlined disclosure in Item 3. Key Information as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“GEHI is not a Chinese operating company but a Cayman Islands holding company with no equity ownership in its variable interest entity, or VIE. We conduct our business in China through (i) our PRC subsidiaries and (ii) the former VIE and the new VIE with which we maintained contractual arrangements. Foreign investment in the education industry and value-added telecommunication industry in China is extensively regulated and subject to numerous restrictions. Accordingly, we historically operated these businesses in China through the former VIE, and relied on contractual arrangements among our PRC subsidiaries, the former VIE and their shareholders to control the business operations of the former VIE. We have entered into agreements with former VIE to terminate the contractual arrangements in March 2022, pursuant to which the previous contractual arrangements were terminated, and we divested our directly operated kindergarten business on April 30, 2022. Pursuant to PRC laws and regulations, ICP license can only be held by companies with an ultimate capital contribution percentage by foreign investor(s) not exceed 50%. Accordingly, in April 2022, we entered into a series of contractual agreements with Zhudou Investment, or the new VIE, and its shareholders and its subsidiaries for licensing concern. See ‘Item 4. Information on the Company—C. Organizational Structure’ for further details. This structure involves unique risks to investors. Chinese regulatory authorities could disallow this structure, which would likely result in a material change in our operations and/or a material change in the value of our securities, including that it could cause the value of our securities to significantly decline or become worthless. For a detailed discussion of risks facing the Company as a result of this structure, see ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure.’ Holders of our ADSs are not holding equity interest in the VIE in China but instead are holding equity interest in Gravitas Education Holdings, Inc., a holding company incorporated and domiciled in the Cayman Islands. Investors of GEHI may never hold equity interests in our Chinese operating companies.”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 5

| 4. | Please disclose whether your auditor is subject to the determinations announced by the PCAOB on December 16, 2021, and whether and how the Holding Foreign Companies Accountable Act and related regulations will affect your company. In this regard, disclose that trading in your securities may be prohibited under the Holding Foreign Companies Accountable Act if the PCAOB determines that it cannot inspect or investigate completely your auditor, and that as a result an exchange may determine to delist your securities. Please revise the disclosure to include a cross-reference to the applicable risk factor. |

In response to the Staff’s comment, the Company respectfully proposes to include the following disclosure in Item 3. Key Information in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“The Holding Foreign Companies Accountable Act

The Holding Foreign Companies Accountable Act, or the HFCAA, was enacted on December 18, 2020. The HFCAA states that if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit our shares or ADSs from being traded on a national securities exchange or in the over-the-counter trading market in the United States. The related risks and uncertainties could cause the value of our ADSs to significantly decline or be worthless. On December 16, 2021, the PCAOB issued a report to notify the SEC of its determination that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. Our auditor, Friedman LLP, the independent registered public accounting firm that issues the audit report included elsewhere in this annual report, as an auditor of companies that are traded publicly in the United States and a firm registered with the PCAOB, is not subject to the determinations announced by the PCAOB issued on December 16, 2021. Our auditor is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess our auditor’s compliance with the applicable professional standards. We cannot assure you whether regulatory authorities would apply additional and more stringent criteria to us after considering the effectiveness of our auditor’s audit procedures and quality control procedures, adequacy of personnel and training, or sufficiency of resources, geographic reach or experience as it relates to the audit of our financial statements. In the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor, then such lack of inspection could cause trading in our securities to be prohibited under the HFCAA ultimately result in a determination by a securities exchange to delist our securities.

Gravitas Education Holdings, Inc.

August 23, 2022

Page 6

On June 22, 2021, the U.S. Senate passed a bill which proposed to reduce the number of consecutive non-inspection years required for triggering the prohibitions under the HFCAA from three years to two. On February 4, 2022, the U.S. House of Representatives passed a bill which contained, among other things, an identical provision. Our ADSs will be prohibited from trading in the United States under the HFCAA, in 2024 if it is later determined that the PCAOB is unable to inspect or investigate completely our auditor, or in 2023 if proposed changes to the law are enacted. The delisting of our ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment. For more details, see ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Our ADSs may be prohibited from trading in the United States under the Holding Foreign Companies Accountable Act, or the HFCAA, if the PCAOB is unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections over our auditor deprives our investors with the benefits of such inspections. The delisting of our ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment.’”

| 5. | Please revise to prominently disclose the entity (including the domicile) in which investors own an interest. Additionally, please disclose that investors may never hold equity interests in your Chinese operating companies. |

In response to the Staff’s comment, the Company respectfully proposes to include the following underlined disclosure in Item 3. Key Information as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“GEHI is not a Chinese operating company but a Cayman Islands holding company with no equity ownership in its variable interest entity, or VIE. We conduct our business in China through (i) our PRC subsidiaries and (ii) the former VIE and the new VIE with which we maintained contractual arrangements. Foreign investment in the education industry and value-added telecommunication industry in China is extensively regulated and subject to numerous restrictions. Accordingly, we historically operated these businesses in China through the former VIE, and relied on contractual arrangements among our PRC subsidiaries, the former VIE and their shareholders to control the business operations of the former VIE. We have entered into agreements with former VIE to terminate the contractual arrangements in March 2022, pursuant to which the previous contractual arrangements were terminated, and we divested our directly operated kindergarten business on April 30, 2022. Pursuant to PRC laws and regulations, ICP license can only be held by companies with an ultimate capital contribution percentage by foreign investor(s) not exceed 50%. Accordingly, in April 2022, we entered into a series of contractual agreements with Zhudou Investment, or the new VIE, and its shareholders and its subsidiaries for licensing concern. See ‘Item 4. Information on the Company—C. Organizational Structure’ for further details. This structure involves unique risks to investors. Chinese regulatory authorities could disallow this structure, which would likely result in a material change in our operations and/or a material change in the value of our securities, including that it could cause the value of such securities to significantly decline or become worthless. For a detailed discussion of risks facing the Company as a result of this structure, see ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure.’ Holders of our ADSs are not holding equity interest in the VIE in China but instead are holding equity interest in Gravitas Education Holdings, Inc., a holding company incorporated and domiciled in the Cayman Islands. Investors of GEHI may never hold equity interests in our Chinese operating companies.”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 7

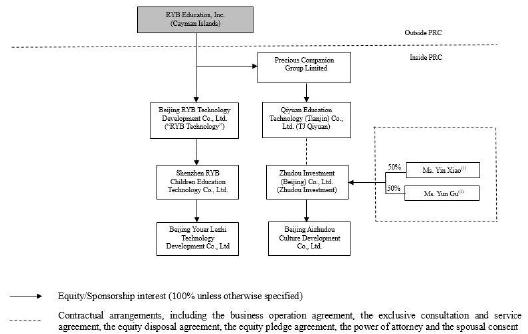

| 6. | Provide early in the summary a diagram of the company’s corporate structure, identifying the person or entity that owns the equity in each depicted entity. With respect to the disclosed contractual arrangements with the VIEs in the diagram to be included here and in Item 4.C on page 85, please revise to use dashed lines without arrows. Additionally, describe all contracts and arrangements through which you claim to have economic rights and exercise control that results in consolidation of the VIE’s operations and financial results into your financial statements. Describe the relevant contractual agreements between the entities and how this type of corporate structure may affect investors and the value of their investment, including how and why the contractual arrangements may be less effective than direct ownership and that the company may incur substantial costs to enforce the terms of the arrangements. Disclose the uncertainties regarding the status of the rights of the Cayman Islands holding company with respect to its contractual arrangements with the VIE, its founders and owners, and the challenges the company may face enforcing these contractual agreements due to legal uncertainties and jurisdictional limits. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the following underlined disclosure in Item 3. Key Information as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed. Where similar disclosure appears in other places of the Form 20-F, conforming changes will be implemented to ensure consistency throughout the annual report.

Gravitas Education Holdings, Inc.

August 23, 2022

Page 8

“A series of contractual agreements, including powers of attorney, exclusive consulting and services agreement, exclusive option agreement, equity disposal agreement, equity interest pledge agreements, business operation agreement, confirmation letter and spousal consent letter, were entered into by and among our wholly owned PRC subsidiaries, the former VIE, and their shareholders. As a result of the contractual arrangements, we have obtained the power to direct the activities of the former VIE and have consolidated the financial results of the former VIE in our consolidated financial statements for the effective period of the respective contractual arrangements. Revenues contributed by the former VIE accounted for 89.2%, 73.0% and 78.8% of our total revenues for the years of 2019, 2020 and 2021, respectively. For more details of these contractual arrangements, see ‘Item 4. Information on the Company—C. Organizational Structure—Contractual Arrangements with the Former VIE and Their Respective Shareholders.’

We, through Qiyuan Education Technology (Tianjin) Co., or TJ Qiyuan, had entered into a series of contractual arrangements with the new VIE and the nominee shareholders of the new VIE following the termination of the former VIE on April 30, 2022. These contractual agreements include exclusive consultation and service agreements, business operation agreements, powers of attorney, equity pledge agreements, exclusive option agreements and spousal consent letters. During the effective period of these contractual arrangements, these contractual arrangements would enable us to: (i) receive the economic benefits that could potentially be significant to the new VIE in consideration for the services provided by our subsidiaries; (ii) direct the activities of the new VIE; and (iii) hold an exclusive option to purchase all or part of the equity interests in and assets of the new VIE when and to the extent permitted by PRC law. For more details of these contractual arrangements, see ‘Item 4. Information on the Company—C. Organizational Structure—Contractual Arrangements with the New VIE and Its Respective Shareholders.’

Gravitas Education Holdings, Inc.

August 23, 2022

Page 9

The following diagram illustrates our corporate structure, including our principal subsidiaries, principal VIE and its principal subsidiaries, and other entities that are material to our business, as of the date of this annual report:

| (1) | Ms. Yin Xiao and Ms. Yun Gu are beneficial owners of the shares of Zhudou Investment and hold 50% and 50% equity interests in Zhudou Investment, respectively. |

However,

the This type of corporate structure may affect investors and the value of their investment. The contractual arrangements

may not be as effective as direct ownership in providing us with control over the VIE and we may incur substantial costs to enforce the

terms of the arrangements. In addition, these agreements have not been tested in China courts. See ‘Item 3. Key Information—D.

Risk Factors—Risks Related to Our Corporate Structure—We rely on contractual arrangements with the VIE and its shareholders

for a large portion of our business operations, which may not be as effective as direct ownership in providing operational control,’

and ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—The shareholders of the

VIE may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.’

There are also substantial uncertainties

regarding the interpretation and application of current and future PRC laws, regulations and rules regarding the status of the rights

of our Cayman Islands holding company with respect to its contractual arrangements with the VIE and its founders and owners shareholders.

It is uncertain whether any new PRC laws or regulations relating to VIE structures will be adopted or if adopted, what they would provide.

As a result, we may face challenges enforcing these contractual arrangements due to legal uncertainties and jurisdictional limits.

Additionally, the PRC regulatory authorities may in the future take a different view towards the compliance status of our Cayman Islands

holding company and its contractual arrangements with the VIE. If we or the VIE is found to be in violation of any existing or future

PRC laws or regulations, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities

would have broad discretion to take action in dealing with such violations or failures. See ‘Item 3. Key Information—D. Risk

Factors—Risks Related to Our Corporate Structure—If the PRC government finds that the agreements that establish the structure

for operating some of our business operations in China do not comply with PRC regulations relating to the relevant industries, or if these

regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties, or be forced

to relinquish our interest in those operations,’ and ‘—Risks Related to Doing Business in China—Our current corporate

structure and business operations may be affected by the newly enacted Foreign Investment Law.’”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 10

| 7. | Please revise to provide a summary of risk factors section, disclose the risks that your corporate structure and being based in or having the majority of the company’s operations in China poses to investors. In particular, describe the significant regulatory, liquidity, and enforcement risks with specific cross-references to the more detailed discussion of these risks in the document. For example, specifically discuss risks arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and that rules and regulations in China can change quickly with little advance notice; and the risk that the Chinese government may intervene or influence your operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China based issuers, which could result in a material change in your operations and/or the value of your securities. Acknowledge any risks that any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. In this regard, we note that the “Summary of Risk Factors” section on page 10 should be moved to earlier in Item 3 and address the above disclosure topics. |

In response to the Staff’s comment, the Company respectfully proposes to include the following underlined disclosure in the “Summary of Risk Factors” section as shown below and move it to earlier in Item 3. Key Information in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“Risks Related to Our Corporate Structure

| ● | GEHI is a Cayman Islands holding company with no equity ownership in the VIE and we conduct our operations in China primarily through (i) our PRC subsidiaries and (ii) the VIE with which we have maintained contractual arrangements. Investors in our ADSs thus are not purchasing equity interest in our operating entities in China but instead are purchasing equity interest in a Cayman Islands holding company. If the PRC government finds that the agreements that establish the structure for operating our business in China do not comply with PRC laws and regulations, or if these regulations or the interpretation of existing regulations change in the future, we and the VIE could be subject to severe penalties or be forced to relinquish our interests in those operations. Our holding company in the Cayman Islands, our PRC subsidiaries, the VIE, and investors of GEHI face uncertainty about potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the VIE and, consequently, significantly affect the financial performance of the VIE and our company as a whole. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government finds that the agreements that establish the structure for operating some of our business operations in China do not comply with PRC regulations relating to the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties, or be forced to relinquish our interest in those operations;’ |

Gravitas Education Holdings, Inc.

August 23, 2022

Page 11

| ● | Substantial uncertainties exist with respect to the interpretation and implementation of the Foreign Investment Law and how it may impact the viability of our current corporate structure, corporate governance and business operations. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—Substantial uncertainties exist with respect to the interpretation and implementation of the Foreign Investment Law and how it may impact the viability of our current corporate structure, corporate governance and business operations;’ |

| ● | We rely on contractual arrangements with the VIE and its shareholders for a large portion of our business operations, which may not be as effective as direct ownership in providing operational control. We rely on the performance by the VIE and its shareholders of their obligations under the contracts to have the power to direct the activities of the VIE. The shareholders of the VIE may not act in the best interests of GEHI or may not perform their obligations under these contracts. Such risks exist throughout the period in which we intend to operate certain portion of our business through the contractual arrangements with the VIE. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We rely on contractual arrangements with the VIE and its shareholders for a large portion of our business operations which may not be as effective as direct ownership in providing operational control;’ |

| ● | Any failure by the VIE or its shareholders to perform their obligations under our contractual arrangements with them would have a material and adverse effect on our business. If the VIE or its shareholders fail to perform their respective obligations under the contractual arrangements, we may have to incur substantial costs and expend additional resources to enforce such arrangements. We may also have to rely on legal remedies under PRC law, including seeking specific performance or injunctive relief, and claiming damages, which we cannot assure you will be effective under PRC law. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—Any failure by the VIE or its shareholders to perform their obligations under our contractual arrangements with them would have a material and adverse effect on our business;’ and |

Gravitas Education Holdings, Inc.

August 23, 2022

Page 12

| ● | The shareholders of the VIE may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition. The shareholders of the VIE may breach, or cause the VIE to breach, or refuse to renew, the existing contractual arrangements we have with them and the VIE, which would have a material adverse effect on our ability to direct the activities of the VIE and receive economic benefits from them. If we cannot resolve any conflict of interest or dispute between us and these shareholders, we would have to rely on legal proceedings, which could result in disruption of our business and subject us to substantial uncertainty as to the outcome of any such legal proceedings. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—The shareholders of the VIE may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.’ |

Risks Related to Doing Business in China

| ● | Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business and operations. The enforcement of laws and rules and regulations in China may change quickly with little advance notice, which could result in a material adverse change in our operations and the value of our ADSs. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business and operations;’ |

| ● | The approval of and filing with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under PRC law, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing. Any failure to obtain or delay in obtaining the requisite governmental approval for an offering, or a rescission of such approval, would subject us to sanctions imposed by the relevant PRC regulatory authority. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The approval of and filing with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under PRC law, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing;’ |

Gravitas Education Holdings, Inc.

August 23, 2022

Page 13

| ● | The PRC government’s significant oversight over our business operation could result in a material

adverse change in our operations and the value of our ADSs. The Chinese government may intervene or influence our operations at any time,

or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in

a material change in our operations and/or the value of our securities. Any actions by the Chinese government to exert more oversight

and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely

hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline

or become worthless. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The

PRC government’s significant oversight over our business operation could result in a material adverse change in our operations and

the value of our ADSs; |

| ● | The recent joint statement by the SEC and PCAOB, proposed rule changes submitted by Nasdaq, and the Holding Foreign Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our offering. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Our ADSs may be prohibited from trading in the United States under the Holding Foreign Companies Accountable Act, or the HFCAA, if the PCAOB is unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections over our auditor deprives our investors with the benefits of such inspections. The delisting of our ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment;’ |

| ● | Uncertainties with respect to the PRC legal system could materially and adversely affect us. Rules and regulations in China can change quickly with little advance notice. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Uncertainties with respect to the PRC legal system could adversely affect us;’ |

| ● | You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions against us or our directors and officers named in the annual report based on foreign laws. Substantially all of our of directors and officers are located in China, and it will be more difficult to enforce liabilities and enforce judgments on those individuals. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions in China against us or our directors and officers named in the annual report based on foreign laws; and’ |

Gravitas Education Holdings, Inc.

August 23, 2022

Page 14

| ● | We may rely on dividends and other distributions on equity paid by our PRC subsidiary to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiary to make payments to us could have a material and adverse effect on our ability to conduct our business. To the extent cash or assets in the business is in the PRC or a PRC entity, the funds or assets may not be available to fund operations or for other use outside of the PRC due to interventions in or the imposition of restrictions and limitations on the ability of us, our subsidiaries, or the consolidated VIEs by the PRC government to transfer cash or assets. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We may rely on dividends and other distributions on equity paid by our PRC subsidiary to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiary to make payments to us could have a material and adverse effect on our ability to conduct our business.’” |

| 8. | We note that you do not appear to have relied upon an opinion of counsel with respect to your conclusions that you have the necessary permissions and approvals to operate your business. If true, state as much and explain why such an opinion was not obtained. Please also explain the basis for your conclusions, such as why you are not required to have a cybersecurity review by the China Securities Regulatory Commission or the Cyberspace Administration of China. Additionally, the disclosure related to permission and approvals should not be qualified by materiality. Please make appropriate revisions to your disclosure. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the underlined disclosure in Item 3. Key Information as shown below and file the consent of its mainland China legal counsel in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“Permissions Required from the PRC Authorities for Our Operations

We

conduct our business in China through our subsidiaries and the VIE in China. Our operations in China are governed by PRC laws and regulations.

As advised by our mainland China legal counsel, as of the date of this annual report, except as otherwise stated

in ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Business—We may not be able to obtain all necessary

approvals, licenses and permits or to make all necessary registrations and filings for our educational and other services in the countries

in which we operate’ and ‘Item 3. Key Information—D. Risk Factors—Risks Related to Our Business—Certain

of the operations by the former VIE may be deemed by PRC government to be carried out by entities beyond their authorized business scope,’

our PRC subsidiaries and VIE have obtained the requisite licenses and permits from the PRC government authorities that are material

for the business operations of our holding company and the VIE in China, including, among others, the private school operation permit

from the local education bureau, the registration certificate for private non-enterprise entities issued by the local civil affairs bureau

and the ICP license. Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement

practice by relevant government authorities, we may be required to obtain additional licenses, permits, filings or approvals for the functions

and services of our platform in the future. For more detailed information, see ‘Item 3. Key Information—D. Risk Factors—Risks

Related to Doing Business in China—We may not be able to obtain all necessary approvals, licenses and permits or to make all necessary

registrations and filings for our educational and other services in the countries in which we operate’ and ‘Item 3. Key

Information—D. Risk Factors—Risks Related to Our Business—Certain of the operations by the former VIE may be deemed

by PRC government to be carried out by entities beyond their authorized business scope.’”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 15

The Company also respectfully proposes to revise and include the following underlined disclosure in the referenced risk factor in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“Our business generates and processes a large amount of data, and we are required to comply with PRC and other applicable laws relating to privacy and cybersecurity. The improper use or disclosure of data could have a material and adverse effect on our business and prospects.

[…]

| · | In June 2021, the Standing Committee of the NPC promulgated the Data Security Law, which took effect

in September 2021. The Data Security Law, among other things, provides for security review procedure for data-related activities

that may affect national security. In July 2021, the state council promulgated the Regulations on Protection of Critical Information

Infrastructure, which became effective on September 1, 2021. Pursuant to this regulation, critical information infrastructure means

key network facilities or information systems of critical industries or sectors, such as public communication and information service,

energy, transportation, water conservation, finance, public services, e-government affairs and national defense science, the damage, malfunction

or data leakage of which may endanger national security, people’s livelihoods and the public interest. In December 2021, the

CAC, together with other authorities, jointly promulgated the Cybersecurity Review Measures, which became effective on February 15,

2022, and replaces its predecessor regulation. Pursuant to the Cybersecurity Review Measures, critical information infrastructure operators

that procure internet products and services must be subject to the cybersecurity review if their activities affect or may affect national

security. The Cybersecurity Review Measures further stipulates that critical information infrastructure operators or network platform

operators that hold personal information of over one million users shall apply with the Cybersecurity Review Office for a cybersecurity

review before any public offering at a foreign stock exchange. As of the date of this annual report, we are not required to have a

cybersecurity review by the CSRC or the CAC. The basis for our conclusion are as follows: (i) no detailed rules or implementation

rules have been issued by any authority; (ii) |

Gravitas Education Holdings, Inc.

August 23, 2022

Page 16

| 9. | Provide a clear description of how cash is transferred through your organization. Disclose your intentions to distribute earnings or settle amounts owed under the VIE agreements for both the former VIE and the new VIE. Quantify any cash flows and transfers of other assets by type that have occurred between the holding company, its subsidiaries, and the consolidated VIEs, and direction of transfer. Describe any restrictions and limitations on your ability to distribute earnings from the company, including your subsidiaries and/or the consolidated VIEs, to the parent company and U.S. investors as well as the ability to settle amounts owed under the VIE agreements. Provide cross-references to the condensed consolidating schedule and the consolidated financial statements. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the underlined disclosure in Item 3. Key Information as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“Cash Flows through Our Organization

GEHI is a holding company with no operations of its own. We conduct our business in China through our subsidiaries and the VIE in China. As a result, although other means are available for us to obtain financing at the holding company level, GEHI’s ability to pay dividends to the shareholders and to service any debt it may incur may depend upon dividends paid by our PRC subsidiaries and license and service fees paid by the VIE. If any of our subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to GEHI. In addition, our PRC subsidiaries are permitted to pay dividends to GEHI only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Further, our PRC subsidiaries and VIE are required to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies. For more details, see ‘Item 3. Key Information—Financial Information Related to the VIE’ and ‘Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Holding Company Structure.’

Gravitas Education Holdings, Inc.

August 23, 2022

Page 17

Under PRC laws and regulations, our PRC subsidiaries and VIE are subject to certain restrictions and limitations with respect to paying dividends or otherwise transferring any of their net assets to us and our U.S. investors as well as to settle amounts owed under the VIE agreements. Remittance of dividends by a wholly foreign-owned enterprise out of China is also subject to examination by the banks designated by State Administration of Foreign Exchange, or the SAFE. The amounts restricted include the paid-up capital and the statutory reserve funds of our PRC subsidiaries and the net assets of the VIE in which we have no legal ownership, totaling US$3.5 million, US$7.2 million and US$13.4 million as of December 31, 2019, 2020 and 2021, respectively. For risks relating to the fund flows of our operations in China, see ‘Item 3. Key Information—Risk Factors—Risks Related to Doing Business in China—We may rely on dividends and other distributions on equity paid by our PRC subsidiary to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiary to make payments to us could have a material and adverse effect on our ability to conduct our business.’

Under PRC law, GEHI may provide funding to our PRC subsidiaries only through capital contributions or loans, and to the VIE only through loans, subject to satisfaction of applicable government registration and approval requirements. For the years ended December 31, 2019, 2020 and 2021, GEHI extended loans with outstanding principal amount of US$55.4 million, US$34.4 million and US$34.4 million, respectively, to our intermediate holding companies and subsidiaries and the former VIE. Further, our PRC subsidiaries received nil, nil, and nil as capital contributions, respectively, and the former VIE received nil, nil and nil as capital or investment, respectively. PRC subsidiaries received US$50.3 million, nil and US$11.5 million from the former VIE for daily operation for the years ended December 31, 2019, 2020 and 2021, respectively. The former VIE received nil, US$52.0 million and nil from our PRC subsidiaries for daily operation for the years ended December 31, 2019, 2020 and 2021, respectively. The former VIE may transfer cash to our PRC subsidiaries by paying services fees according to the contractual agreements. The former VIE paid our PRC subsidiaries service fees US$10.8 million, US$4.5 million and US$4.9 million for the years ended December 31, 2019, 2020 and 2021, respectively. We currently have no cash management policies that dictate how funds are transferred between us, our subsidiaries, the consolidated VIEs or investors. For more details, see ‘Item 3. Key Information—Financial Information Related to the VIE.’

Gravitas Education Holdings, Inc.

August 23, 2022

Page 18

GEHI has not declared or paid any cash dividends, nor does it have any present plan to pay any cash dividends on our ordinary shares in the foreseeable future. Additionally, GEHI has no intention to distribute earnings, but our PRC subsidiaries have settled and will settle amounts with the VIEs under the VIE agreements for both the former VIE and the new VIE. We currently intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business. See ‘Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Dividend Policy.’ For PRC and United States federal income tax considerations of an investment in our ADSs, see ‘Item 10. Additional Information—E. Taxation.’

| 10. | Please revise this section, in the summary risk factors and risk factors sections to state that, to the extent cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds or assets may not be available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of restrictions and limitations on the ability of you, your subsidiaries, or the consolidated VIEs by the PRC government to transfer cash or assets. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the underlined disclosure in the summary risk factors in Item 3. Key Information as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“Risks Related to Doing Business in China

[…]

| ● | We may rely on dividends and other distributions on equity paid by our PRC subsidiary to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiary to make payments to us could have a material and adverse effect on our ability to conduct our business. To the extent cash or assets in the business is in the PRC or a PRC entity, the funds or assets may not be available to fund operations or for other use outside of the PRC due to interventions in or the imposition of restrictions and limitations on the ability of us, our subsidiaries, or the consolidated VIEs by the PRC government to transfer cash or assets. See ‘Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We may rely on dividends and other distributions on equity paid by our PRC subsidiary to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiary to make payments to us could have a material and adverse effect on our ability to conduct our business.’” |

Gravitas Education Holdings, Inc.

August 23, 2022

Page 19

The Company also respectfully proposes to revise and include the following underlined disclosure in the referenced risk factor in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“We are a Cayman Islands holding company and we rely principally on dividends and other distributions on equity from our PRC subsidiary for our cash requirements, including for services of any debt we may incur. Our PRC subsidiary’s ability to distribute dividends is based upon its distributable earnings. Current PRC regulations permit our PRC subsidiary to pay dividends to its respective shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, each of our PRC subsidiary, the VIE and its subsidiaries are required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Our PRC subsidiary as a foreign invested enterprise, or FIE, is also required to further set aside a portion of its after-tax profit to fund an employee welfare fund, although the amount to be set aside, if any, is determined at its discretion. These reserves are not distributable as cash dividends. If our PRC subsidiary incurs debt on their own behalf in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments to us. To the extent cash or assets in the business is in the PRC or a PRC entity, the funds or assets may not be available to fund operations or for other use outside of the PRC due to interventions in or the imposition of restrictions and limitations on the ability of us, our subsidiaries, or the consolidated VIEs by the PRC government to transfer cash or assets. Any limitation on the ability of our PRC subsidiary to distribute dividends or other payments to their respective shareholders could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our businesses, pay dividends or otherwise fund and conduct our business.”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 20

| 11. | To the extent you have cash management policies that dictate how funds are transferred between you, your subsidiaries, the consolidated VIEs or investors, summarize the policies in this section, and disclose the source of such policies (e.g., whether they are contractual in nature, pursuant to regulations, etc.); alternatively, state in this section that you have no such cash management policies that dictate how funds are transferred. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the underlined disclosure in Item 3. Key Information as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“Under PRC law, GEHI may provide funding to our PRC subsidiaries only through capital contributions or loans, and to the VIE only through loans, subject to satisfaction of applicable government registration and approval requirements For the years ended December 31, 2019, 2020 and 2021, GEHI extended loans with outstanding principal amount of US$55.4 million, US$34.4 million and US$34.4 million, respectively, to our intermediate holding companies and subsidiaries, and VIE received nil, nil and nil as capital or investment, respectively. We do not have cash management policies that dictate how funds are transferred between us, our subsidiaries, the consolidated VIEs or investors as of the date of this annual report.”

Item 3(d). Risk Factors, page 10

| 12. | In light of recent events indicating greater oversight by the Cyberspace Administration of China (CAC) over data security, particularly for companies seeking to list on a foreign exchange, please revise your disclosure to explain how this oversight impacts your business and to what extent you believe that you are compliant with the regulations or policies that have been issued by the CAC to date. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the following underlined disclosure in the referenced risk factor in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“Our business generates and processes a large amount of data, and we are required to comply with PRC and other applicable laws relating to privacy and cybersecurity. The improper use or disclosure of data could have a material and adverse effect on our business and prospects.

[…]

We

are subject to various regulatory requirements relating to cybersecurity and data privacy, including, without limitation, the PRC Cybersecurity

Law. We are required by these laws and regulations to ensure the confidentiality, integrity, availability, and authenticity of the information

of our users. However, the The PRC regulatory and enforcement regime with regard to data security and data

protection is evolving and may be subject to different interpretations or significant changes, resulting in uncertainties about the

scope of our responsibilities in that regard. Moreover, different PRC regulatory bodies, including the Standing Committee of the NPC,

the Ministry of Industry and Information Technology, or the MIIT, the CAC, the MPS and the SAMR, have enforced data privacy and protections

laws and regulations with varying standards and applications. See ‘Item 4. Information on the Company—B. Business Overview—Regulation—Regulations

Relating to Internet Information Security and Privacy Protection.’ The following are examples of certain recent PRC regulatory activities

in this area …

Gravitas Education Holdings, Inc.

August 23, 2022

Page 21

[…]

Many of the data-related legislations

are relatively new and certain concepts thereunder remain subject to interpretation by the regulators. If any data that we possess belongs

to data categories that are subject to heightened scrutiny, we may be required to adopt stricter measures for protection and management

of such data. In terms of our usage of mobile app, website and system, we received several notices from the relevant public security department

in 2019 and 2020 (the “2019 and 2020 Notices”), which required us to rectify the privacy policy of our mobile app,

the collection and the usage of personal information on our mobile app, and the security of our website and system. We have completed

the rectification according to the 2019 and 2020 Notices aforementioned notices and submitted a written rectification

report to the relevant public security department. These notices and rectifications did not have any material impact to our business operations.

As of the date of this annual report, (i) we have not been subject to any material fines or administrative penalties, mandatory rectifications, or other sanctions by any competent regulatory authorities in relation to the infringement of cybersecurity and data protection laws and regulations; (ii) we have not found that there is any material leakage of data or personal information or violation of cybersecurity, data protection and privacy laws and regulations by us which will have a material adverse impact on our business operations; (iii) there had been no material cybersecurity or data protection incidents or infringement upon the rights of any third parties, or other legal, administrative or governmental proceedings pending or, to the best of the knowledge of our Company, threatened against or relating to our Company. Furthermore, based on the facts that, (i) the Cybersecurity Review Measures were newly adopted and the Draft Regulations have not been formally adopted, and the implementation and interpretation of both are subject to uncertainties, and (ii) we have not been involved in any investigations on cyber security review made by the CAC on such basis, nor have we received any inquiries, notices, warnings, or sanctions in such respect, we are of the view that such regulations do not have a material adverse impact on our business operations and financial performance as of the date of this annual report, and will not affect our compliance with laws and regulations in any material aspects as of the date of this annual report. As of the date of this annual report, with the exception of the 2019 and 2020 Notices, we have not received any cybersecurity, data security and personal data protection related inquiries from any competent PRC regulatory authorities. We are of the view that we are in material compliance with the existing PRC laws and regulations on cybersecurity, data security and personal data protection, and the existing laws and regulations in cybersecurity, data security and personal data protection will not have a material adverse impact on our business operations. As there might be newly issued explanations or implementation rules on the existing regulations, laws and opinions or the draft measures mentioned above that may become effective, we will actively monitor future regulatory and policy changes to ensure strict compliance with all applicable laws and regulations.”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 22

| 13. | To the extent that any of your officers and directors are located in China, Macau or Hong Kong, please add a risk factor that addresses the difficulty of bringing actions against these individuals and enforcing judgments against them. |

In response to the Staff’s comment, the Company respectfully proposes to include the underlined disclosure in the referenced risk factor as shown below in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“You may experience difficulties

in effecting service of legal process, enforcing foreign judgments or bringing actions in China against us or our directors and officers

management named in the annual report based on foreign laws.

We are an exempted

company incorporated under the laws of the Cayman Islands, we conduct substantially most of our operations in China and substantially

most of our assets are located in China. In addition, substantially all of our directors and officers all our senior executive

officers reside within China for a significant portion of the time and most are PRC nationals. As a result, it may be difficult

for our shareholders to effect service of process upon us or those persons inside mainland China. It will also be more difficult to

bring actions against these individuals and to enforce judgments against them.

In addition, China does not have treaties providing for the reciprocal recognition and enforcement of judgments of courts with the Cayman Islands and many other countries and regions. As such, the PRC courts will review and determine the applicability of the reciprocity principle on a case-by-case basis and the length of the procedure is uncertain. Further, according to the PRC Civil Procedures Law, courts in the PRC will not enforce a foreign judgment against us or our directors and officers if they decide that the judgment violates the basic principles of PRC law or national sovereignty, security or public interest. Therefore, recognition and enforcement in China of judgments of a court in any of these non-PRC jurisdictions in relation to any matter not subject to a binding arbitration provision may be difficult or impossible.

Gravitas Education Holdings, Inc.

August 23, 2022

Page 23

Under the PRC Civil Procedures Law, foreign shareholders may originate actions based on PRC law against a company in China for disputes if they can establish sufficient nexus to the PRC for a PRC court to have jurisdiction, and meet other procedural requirements. It will be, however, difficult for U.S. shareholders to originate actions against us in the PRC in accordance with PRC laws because we are incorporated under the laws of the Cayman Islands and it will be difficult for U.S. shareholders, by virtue only of holding the ADSs or ordinary shares, to establish a connection to the PRC for a PRC court to have jurisdiction as required under the PRC Civil Procedures Law. In addition to the aforesaid substantial uncertainties, the foreign shareholders seeking the enforcement of a foreign judgement in the PRC courts could incur substantial legal and other costs that may be material to the shareholders. Shareholders could potentially spend a considerable amount of time and other resources to go through the recognition and enforcement procedure, which may be a significant burden for the shareholders, but with no assurance of ultimate success.”

If the PRC government finds that the agreements that establish the structure for operating some of our business operations in China, page 30

| 14. | Please revise to acknowledge that if the PRC government determines that the contractual arrangements constituting part of the VIE structure do not comply with PRC regulations, or if these regulations change or are interpreted differently in the future, your securities may decline in value or become worthless if the determinations, changes, or interpretations result in your inability to assert contractual control over the assets of your PRC subsidiaries or the VIEs that conduct all or substantially all of your operations. |

In response to the Staff’s comment, the Company respectfully proposes to include the following underlined disclosure in the referenced risk factor in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“In the opinion of our mainland

China PRC legal counsel, Commerce & Finance Law Offices, (i) the ownership structure of the VIE in

China and our subsidiaries are not in violation of applicable PRC laws and regulations currently in effect; and (ii) the contractual

arrangements between our subsidiaries, the VIE and their shareholders governed by PRC laws and regulations are valid, binding on each

party there-to, and will not result in any violation of applicable PRC laws and regulations during the effective period of the respective

contractual arrangements. However, our mainland China PRC legal counsel has also advised us that there are substantial

uncertainties regarding the interpretation and application of current and future PRC laws and regulations. Accordingly, the PRC regulatory

authorities may take a view that is contrary to the opinion of our mainland China PRC legal counsel. In the

event that the PRC regulatory authorities take a contrary view to our mainland China legal counsel, or if the applicable PRC laws and

regulations change or are interpreted differently in the future, the contractual arrangements constituting part of the VIE structure may

not comply with PRC regulations. Furthermore, our securities may decline in value or become worthless if the determinations, changes,

or interpretations result in our inability to assert contractual control over the assets of our PRC subsidiaries or the VIEs that conduct

all or substantially all of our operations.”

Gravitas Education Holdings, Inc.

August 23, 2022

Page 24

Item 4.C Organizational Structure

Contractual Arrangements with the Former VIE and Their Respective Shareholders, page 85

| 15. | We note your disclosure regarding the disposal of the former VIE, which included Beijing RYB Children Education Technology Development Co., Ltd., Beiyao Technology Development Co., Ltd., and their subsidiaries. Please revise to provide more information regarding the impetus for this reorganization and any material financial impact this may have upon the company. |

In response to the Staff’s comment, the Company respectfully proposes to revise and include the following underlined disclosure in the referenced section in its future Form 20-F filings, subject to updates and adjustments to be made in connection with any material development of the subject matter being disclosed:

“In March 2022, we entered into agreements, including the VIE termination agreement by and among RYB Technology, Beijing RYB and its shareholders, to terminate the aforementioned contractual arrangements with the former VIE. RYB Technology no longer had the contractual power to direct the activities of the former VIE from April 30, 2022, thereby divesting the directly operated kindergarten business on April 30, 2022, or the ‘Divestiture.’ The Divestiture was mainly motivated by a strategic upgrade in our business. We planned on transitioning our business model to become an educational services output platform and would derive significant revenue through such transition. An aggregate amount of RMB158.5 million will be paid in installments to our subsidiaries as compensation for the termination of VIE agreements. For detailed information regarding all material financial impacts related to the divestiture, see ‘Item 5. Operating and Financial Review and Prospects—A. Operating Results—Financial Impact by the Divestiture’ and ‘Notes to Consolidated Financial Statements for the Years Ended December 31, 2019, 2020 and 2021—26. Subsequent Event.’”

* * *

| Very truly yours, | |

| /s/ Hao Gu | |

| Hao Gu | |

| Chief Financial Officer |

| cc: | Yanlai Shi, Chief Executive Officer, Gravitas Education Holdings, Inc. Yuting Wu, Esq., Partner, Skadden, Arps, Slate, Meagher & Flom LLP |